![]()

Source: SweeneyToddMovie.com

What choice do banks have but to lend?

The administration unveiled its Homeowner Affordability and Stability Plan [HASP], to the praise of TARP recipients. Other investors remain more guarded, and the prices of major financial stocks continue their steady descent to an April 10th “touchdown”, or wipeout. If, or as, these firms are wiped out, their securitized assets can be deconstructed, and transferred to community banks.

Homeowner Affordability and Stability Plan, HASP

As detailed in DanskeBank’s Obama’s Housing Plan, HASP intends to:

- Improve refinancing access;

- Modify mortgages that are at risk of default,

- Support low mortgage rates through Fannie & Freddie.

- Refinancing access will be improved by permitting homeowners with existing loans backed by Fannie or Freddie, to refi even if their LTV has risen above 80% due to home value declines.

- Modifications will be supported by $75 billion drawn from TARP, as lenders are encouraged to reduce monthly mortgage payments for “at risk” homeowners to 31% of borrowers’ gross income. Costs will be shared between mortgage holders and the government.

- The Treasury will attempt to lower mortgage rates by doubling its preferred stock investments in each GSE, from $100 billion/GSE to $200 billion./GSE. In addition, GSE’s retained mortgage portfolios will be increased by $50 billion, to $900 billion.

EARLY REACTION TO HASP

TARP recipients praised the plan, with one participant announcing:

“We applaud:

- The focus on making monthly payments affordable for borrowers

- The creation of uniform national standards for mortgage modification;

- The partnership with government to reduce [borrowers’] interest rates and payments;

- The expanded ability of borrowers to take advantage of … refinancing;

- The inclusion of financially distressed borrowers even before they are delinquent; and

- The use of counseling for borrowers with the highest debt ratios.”

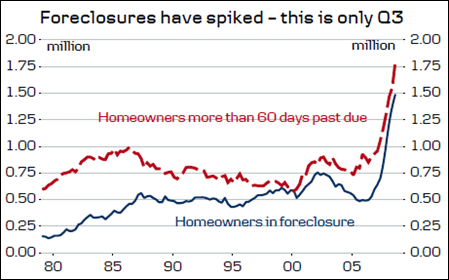

Figure 1: 60 Day Delinquencies and Foreclosures

Source: DanskeBank, Obama’s Housing Plan, 19 Feb 2009.

Relatively disinterested institutional investors were more guarded. DanskeBank drew particular attention to the recent foreclosure spike (see Figure 1, above), as it cautioned:

- The US housing market continues to struggle and the rise in foreclosures is putting additional downward pressure on home prices. [While] it is … positive that the US government is now targeting foreclosures directly… it remains to be seen whether the plan will ultimately have a major effect on prices and activity in the housing market.

Source: DanskeBank, Obama’s Housing Plan, 19 Feb 2009.

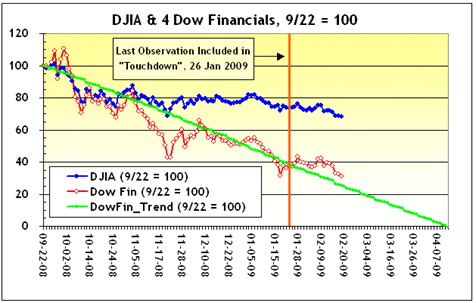

As of mid-day Feb 19, the new administration’s announced initiatives, including HASP, had not yet slowed the steady decline in the top financial stocks included in the Dow Jones Industrial Average. (See my prior Touchdown – When Do Financial Stocks Hit Zero, for the details).

Figure 2: Financials Still On Track for April 10th ‘Touchdown’

Since the important 23 Sep 2008 date noted by Professor John Taylor of Stanford (see my Liquid Plumber), the financials’ price-weighted average index (of American Express, Bank of America, Citigroup, and JPMorgan) has declined by almost seventy percent- and is still on track with my “Touchdown” line (see Figure 2).

WHAT HAPPENS IF THE TOP IS GONE?

If the (previously) unthinkable happens, and the large banks are wiped out (perhaps on or about April 10th) – what happens next?

Before considering an answer, let’s get a sense of how ‘top heavy’ the top actually is, using data from the FDIC’s Quarterly Banking Profile.

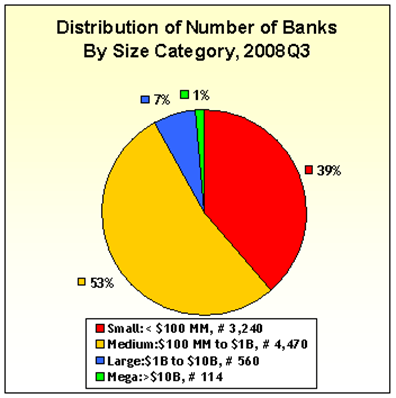

Figure 3: Distribution of Number of Banks, 2008Q3

Source: FDIC Quarterly Banking Profile

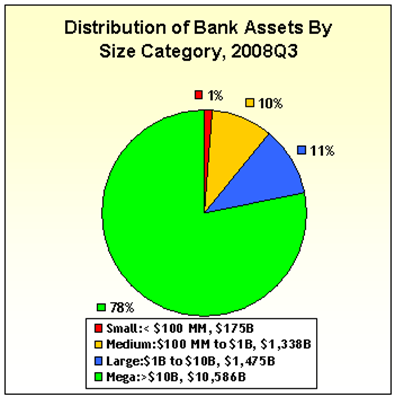

Figure 4: Distribution of Bank Assets, 2008Q3

Source: FDIC Quarterly Banking Profile

As Figures 3 and 4 indicate (above), there are a large number of very small banks as well as a very small number of large banks.

For example, the largest “Mega” banks, account for only 1% of the total number of banks, but hold 78% of the assets. Alternatively, 39% of the banks are very small, yet they hold about 1% of all bank assets.

Unfortunately, the small number of large banks has done a poor job with their disproportionate share of the industry’s assets.

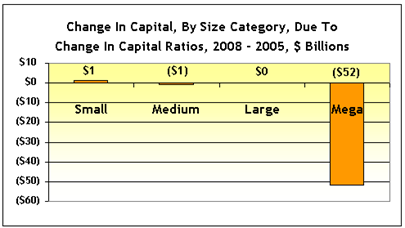

Over the last three years (2005 to 2008Q3), the FDIC figures indicate that the aggregate capital of small, medium, and large banks remained virtually unchanged, while that of large banks sharply eroded.

Figure 5: Change in Capital By Size Category, 2008 - 2005

Source: FDIC Quarterly Banking Profiles, 2008Q3 & 2005Q4, and

Author’s Calculations

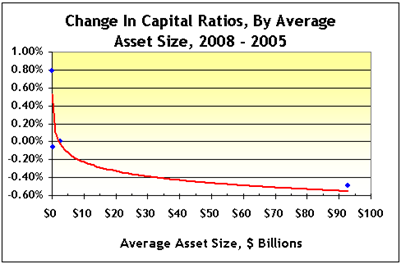

The figure above depicts the change in capital, by category, in billions of dollars. If we re-express the change in capital as a percentage of assets, and plot by the average asset size each category, then we get the following interesting chart (Figure 6, below).

I’ve drawn the red line to emphasize that, over the last three years, if you wanted to find a profitable bank, then you should look among the small. In fact, our limited [!] data suggest that banks shouldn’t get much bigger than 2 or 3 billion in assets, tops.

Figure 6: Change in Capital Ratios By Size Category, 2008 - 2005

Source: FDIC Quarterly Banking Profiles, 2008Q3 & 2005Q4, and

Author’s Calculations

So, what happens if the top is gone? Writing earlier this week, Chris Whalen of Institutional Risk Analytics made the following suggestion:

- The Treasury should begin a systematic process [to acquire] … all of the extant toxic securitizations, transfer ownership of these assets to the Deposit Insurance Fund and then use the receiver powers of the FDIC to reorganize the … [securities].

- Once the FDIC gains legal custody of the collateral, it can then sell these assets through the resolution process now ongoing with financing backed by the Fed.

- Our preference is to see these loans sold to community banks with branches near the property, a move that would immediately enhance the quality of these credits and also make modification/refinancing more practical. [emphasis added]

Source: Chris Whalen, Institutional Risk Analytics - Too Big to Bail: Lehman Brothers is the Model for Fixing the Zombie Banks, 18 Feb, 2009.

It’s that “simple”. You just have to take a little off the top.

- - - - - - - - - - -

![]()

I used to work with numbers for a living. I’m trying to stay sharp as I continue my search for a new job or at least my next idea. Till next time.

REFERENCES

![]()

![]()

![]()

Ira Artman, Sterling Slivers – Touchdown, 26 Jan 2009 & Liquid Plumber, 22 Jan 2009.

Signe Roed-Frederiksen & Peter Possing Andersen, DanskeBank – Obama’s Housing Plan, 19 Feb 2009.

Chris Whalen, Institutional Risk Analytics - Too Big to Bail: Lehman Brothers is the Model for Fixing the Zombie Banks, 18 Feb 2009.

8 responses so far ↓

1 Ira Artman’s Sterling Slivers: A Little Off The Top, Heads Up On Nationalization | Foreclosures For Profit // Feb 19, 2009 at 9:27 pm

[...] Continued here: Ira Artman’s Sterling Slivers: A Litt&… [...]

2 Lia // Feb 19, 2009 at 11:04 pm

Does HASP Homeowner Affordability and Stability Plan have any relation to the new TARP proposal called financial stability plan?

3 Ira Artman’s Sterling Slivers: Our Lives On The D-List, Financial Stocks On The Small Screen // Feb 21, 2009 at 1:08 pm

[...] I know I’ve also said that Friday, 10 April 2009 will be important (see Touchdown or A Little Off The Top), yesterday was just as critical. Here’s [...]

4 Economic Principals » Blog Archive » Late Starter // Feb 22, 2009 at 3:51 pm

[...] mood of financial markets, and an incisive graphic depicting the isolation of the megabanks, see Take a Little Off the Top, by mortgage trader-turned-analyst Ira [...]

5 Dave Quimby // Feb 23, 2009 at 8:25 pm

Ira,

It seems that you are very pessimistic. Governments can only “muddle through”, even in the best of times. They aren’t designed for crisis management and their staffs are inherently risk averse. That is why events seem to be driving policy; probably because they are.

I am very disgusted with the political elites. Good article on Bloomberg online today about the Cambridge, MA (MIT, Harvard) and Ivy League backgrounds, uniformly, among all of the key players.

I don’t know if you saw the CNBC clip with Rick Santelli last week. Gibbs’ response was really condescending and smug (comment about not listening to derivatives traders). Good way to (I hope) dry up campaign contributions. Clearly, Santelli hit a nerve regarding fundamental fairness, a sense of responsibility, and having individuals accept the consequences of their actions. Surprising.

Hope you are well. Be of good cheer; we will get through this. At some point, somthing has to give. Take care.

Regards, Dave Quimby

6 Articles About Everything » Blog Archive » Like Sands Through the Hourglass // Feb 24, 2009 at 3:35 am

[...] Ira points out that not exclusive hit the DOW financials (AMEX, BofA, Citigroup and JPMorgan) been on instruction for an April 10th touchdown of ZERO (essentially a rank wipeout of ordinary hit value) they have, as of terminal weekday as an aggregative average, dropped beneath for the prototypal time. [...]

7 Like Sands Through the Hourglass | Photomaniacal // Mar 3, 2009 at 11:07 pm

[...] Ira points out that not only have the DOW financials (AMEX, BofA, Citigroup and JPMorgan) been on course for an April 10th touchdown of ZERO (essentially a complete wipeout of common stock value) they have, as of last Friday as an aggregate average, dropped below $10 for the first time. [...]

8 Ira Artman’s Sterling Slivers: No News Is & No News & Banks, Home Prices, and Home Sales Are Just Fine // Apr 22, 2009 at 6:07 am

[...] The financial market dislocation was NEVER a problem with the “vast majority of banks.” The problems were, and are, confined to the largest banks, as I described earlier in Follow The Money and A Little Off The Top. [...]

Leave a Comment