![]()

The Independent: Oldest Jawbone Found In Spain

Jawbone: To urge voluntary compliance with

official wishes or guidelines (dictionary.com).

Thursday’s RealtyTrac® press release said a mouthful:

- 04-16-09: RealtyTrac’s US Foreclosure Market Report™ for 2009Q1, … shows that foreclosure filings — default notices, auction sale notices and bank repossessions — were reported on 803,489 properties in the first quarter, a 9% increase from the previous quarter and an increase of nearly 24% from 2008Q1. One in every 159 U.S. housing units received a foreclosure filing during the quarter.

- Foreclosure filings were reported on 341,180 properties in March, a 17% increase from the previous month and a 46% increase from Mar 2008. The March and 2009Q1 totals were the highest monthly and quarterly totals since … [the first] report in Jan 2005…

- “In …March we saw a record level of foreclosure activity — the number of households that received a foreclosure filing was more than 12 percent higher than the next highest month on record. [This] … suggests that many lenders and servicers were holding off on … foreclosures due to industry moratoria and legislative delays,” said [the] …chief executive officer of RealtyTrac. “… It’s very likely that we’ll see the number of REOs increase again now that most of the moratoria have been lifted.

I’m chewing this over because an astute reader of Greed, Fear, and Loathing asked the following question:

- What would the model [developed in Greed, Fear, and Loathing] suggest for the annual change in RPX if foreclosures were reduced to their long-term level, and everything else - including unemployment - was unchanged?

Here’s my answer.

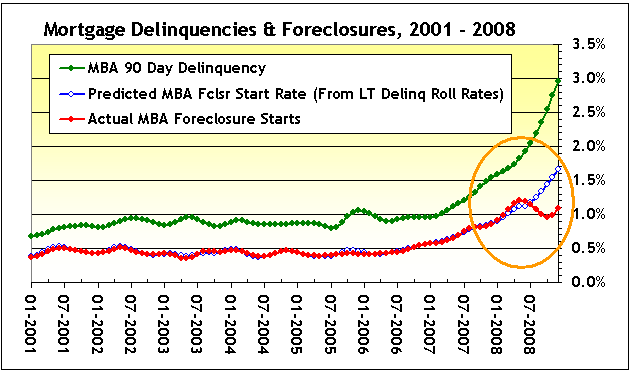

- The long-term average foreclosure start rate, using MBA data ranging from 1979 – 2008, is about 0.35%.

- YE2008 MBA foreclosure starts, at about 1.10%, were more than three times the long-term average. This figure is low. (See Figure 1, below, red line.)

- It is “low” because it is inconsistent with historical delinquency rates, and transition factors, or “roll rates” derived from the relationship between delinquency “buckets” in each month with delinquency rates observed in subsequent months. Example: 60 days past due in February, relative to 90 days past due in March.

- It is “low” due to a combination of legislative & regulatory pressure, and executive jawboning.

- In the absence of jawboning & legislative pressure, foreclosure starts would have been about 1.65%. (See Figure 1, below, blue line.)

- This can be seen in the following chart:

Figure 1: Actual & ‘Predicted’ (From Roll Rates) Foreclosure Starts, Actual 90 Day Delinquencies

So – what IF foreclosures were reduced to their long-term average, and everything else (affordability and unemployment) was unchanged – what would happen to home prices?

- If foreclosure starts were reduced to 0.35%, then the model “says” that the decline in RPX Comp would drop from -23+% to -2%.

But, and here’s an important observation – the requested scenario is a simplified version (more or less) of what you would expect to see if you had:

- Foreclosure jawboning (or “moratoria”); and

- Otherwise generally ineffective or misdirected macro or monetary policies. Example – policies that were inordinately concerned with “saving the banks, rather than the economy” (Paraphrasing Nobel Laureate Joseph Stiglitz, interviewed today on Bloomberg Radio.)

Sound familiar? So let’s say we had jawboning, and little else that really mattered. What happens next?

- Let’s suppose that non-jawboned delinquency doesn’t get any worse from YE2008, and that we modify ALL of the increase in foreclosures from their non-jawboned expectation of 1.65%, and the long-term average of 0.35%. This fantastically optimistic assumption means we would modify 1.30% of all loans, = 1.65% - 0.35%.

- Then, within 9 months (remember, ineffective other policies assumption/ Professor Stiglitz is right) about 60% of these modified loans will redefault (see Barclays’ analysis discussed in my Why Bother?)

- Then the “steady state” foreclosure figure will become:

Total Foreclosure Starts

= (0.35% [Long Term Average]) + (60% x 1.30% from redefaults);

= 0.35% + 0.78% = 1.13%.

- This is not that different from “jawboned” foreclosure start rate of about 1.10% at YE ‘08; and model would produce continued –20+% drops in home prices.

- To put it another way - while waiting for the federal mod programs to be announced, servicers held off on foreclosures. This is reflected in the relatively low foreclosure start rate of about 1.10% seen at YE ‘08.

- If one assumes that the economy and unemployment do NOT recover, and that foreclosures are “addressed” by mod programs (and little else), then the long-term foreclosure rate (taking into account redefaults of the mods, see above) will quickly re-approach the recently unprecedented YE ‘08 levels. This will place continued pressure on home prices.

- Since we are (as noted in Greed, Fear, and Loathing) more or less at point where prices are “fair” relative to income, it is hard to conceive that there might be continued downward price pressure, making real estate REALLY cheap. But given how high things went on the way up, it’s hard to rule out a similar over-correction on down side.

Is that a kick in the teeth, or what?

- - - - - - - - - - -

![]()

I used to work with numbers for a living. I’ll try to keep smiling as I look for a new job, or at least my next idea. Till next time.

2 responses so far ↓

1 Ira Artman’s Sterling Slivers: Foreclosure Zombies of Mass Destruction // Apr 19, 2009 at 7:38 am

[...] modification programs (in which more than half of the “saved” will eventually succumb). See my Jawbone for the [...]

2 Mortgage Markets: Wells Warehouse Lending, Bank United Countdown, Affordability vs. Economy, Ira Artman Jawbones Foreclosures, Jeffries Resecuritization // Apr 20, 2009 at 4:32 am

[...] Ira Artman’s Sterling Slivers: Jawbone - Whither Foreclosures? - What will happen to home prices and foreclosures if ineffective macro policies follow the expiring foreclosure moratoria? A toothy analysis.———— [...]

Leave a Comment